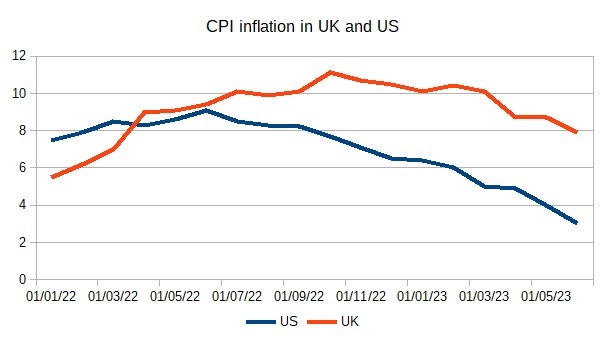

If you wanted to be

optimistic about UK inflation and interest rates, then at first sight

looking at the US might help. Here is inflation in both countries

since the start of 2022.

US inflation peaked

in June last year at 9.1%, and at first its fall from this peak was

slow. By February 2023, eight months after the peak, it had fallen by

only just over 3% to 6.0%. In the UK inflation peaked four months

later than the US, at 11.1% in October 2022. Eight months later, in

June 2023, it had also fallen gradually by around 3% to 7.9%. However

in recent months US inflation has been falling quite rapidly, and in

June it was only 3%. Might UK inflation also begin to fall rapidly?

Are we following the US with a lag of around 4 months?

The way the central

bank has behaved in both countries tells a similar story, with the UK

lagging behind the US in raising rates.

Although inflation

was pretty high at the beginning of 2022, central banks had kept

interest rates low because they expected the increase in inflation to

be temporary and they wanted to protect the recovery from the

pandemic. But from mid-2022 the US Fed increased rates faster than

the Bank of England, and that has helped ensure US inflation is now

falling rapidly. (Quite how much it has helped is another question.)

UK inflation is

indeed expected to fall quite quickly in the UK in the next few

months. The Bank of England’s latest forecast is for inflation to

be below 5% by the last quarter of this year. However if that

suggests to you that interest rates will soon start to come down, you

will be disappointed. Once again a look at the US is instructive.

Despite inflation falling to 3%, the Fed raised interest rates at

their last meeting. The Bank too has said that rates will stay high

for some time. If the inflation outlook is improving, why are rates

staying high?

The answer lies in

the labour market, which in both countries still looks tight. In both

countries wage inflation is still well above what would normally be

regarded as consistent with a 2% inflation target. Here is a

comparison of wage inflation in the UK and US. (For the UK I have

shown a three month rate rather than the usual year on year rate to

better pick up possible turning points, and I have used the Atlanta

Fed Wage Growth tracker for the US. Official

US data on wages shows a similar picture.)

In the US wage

inflation reached a peak in the middle of last year, but falls since

then have been modest. In the UK we cannot be sure that wage

inflation has peaked. In both cases, but particularly in the UK, this

rate of growth in earnings is well above what would be consistent

with 2% inflation. (Something between 3% and 4% would be consistent

with 2% inflation over time.)

As I noted in a

recent

post, you can tell two very different stories about

what is currently happening. In the first story, wage inflation is

high because price inflation has been high, and so once price

inflation starts falling so will wage inflation. In this story, the

inflation problem will be largely self-correcting, and what we are

seeing now is the ‘second round’ effects of a very large but

temporary inflation hike. [1] The second story acknowledges the

temporary inflation hike, but says there is a second problem arising from the pandemic recovery that requires a policy reaction. This

second problem is a tight labour market.

Until the beginning

of last year, central banks believed in the first story. But since

then in both countries the data has suggested a persistently tight

labour market, and it is this that is the main reason why interest

rates have increased. As ever with macroeconomic data, there is a lot

of debate about how reliable any particular labour market indicator

might be (see

this for the US, for example), but the key question is

how tight the market is, rather than is it tight at all.

Where the two

countries differ greatly, however, is in the principle reason why the

labour market is tight, and therefore why wage inflation is high. In

the US it is a story of economic success, with a very strong recovery

from the pandemic. (See the final

chart in this post.) In part this is because fiscal

policy supported the recovery, rather than (in most of Europe) just

supporting the economy during the recession. In contrast the UK has

had a terrible recovery from the pandemic, with GDP per capita still

below pre-pandemic levels. The tight labour market in the UK is the

result of a contraction in labour supply rather than an increase in

labour demand, where causal factors include health problems createdby NHS underfunding and labour shortages as a result of Brexit in

some sectors.

Over the next few

months, therefore, interest rate decisions will focus on what is

happening to wage inflation much more than what is happening to price

inflation. As in the US, in the UK we may find that although price

inflation starts coming down quickly, nominal interest rates will not

start coming down and may even rise. As I emphasised here, what makes

interest setting hard is trying to judge whether you have done enough

when there are considerable lags before higher interest rates have their full impact on activity, and therefore the labour market and wage

inflation. [2]

Perhaps the most

important factor behind the Bank of England’s decision to raise

interest rates last week was this chart, shown at the MPC press

conference.

The solid white area

represents the output of various models of year on year wage growth,

and the white line is the actual data plus the Bank’s forecast for

year on year wage inflation. The models (based on inflation

expectations and various measures of labour market pressure) are

suggesting wage inflation should have started falling this year, but

the actual data hasn’t. The Bank’s/MPC’s reaction is to assume

that wage inflation will continue to be above the models’

predictions, and as a result to tighten policy. [3]

What is clear is

that the UK is entering a new phase of this inflationary period

(which the US has been in for several months), where the focus shifts

from energy and food prices and large cuts in real incomes to the

labour market and positive real wage growth. [4] In the UK average private sector wage inflation has almost caught up with price inflation. The key issue now

becomes whether, as price inflation falls, wage inflation will also

do so, allowing interest rates to stop increasing and start falling.

[1] You could call

this a price-wage spiral, but I wouldn’t. ‘Spiral’ is one of

those

words often used in the 1970s that implies an

explosive process, whereas today is a very different world. The idea

behind the first story about current inflation is for periods where either price or wage inflation lead the other, but both naturally decrease over time.

[2] A lot of popular

discussion about inflation on the left focuses on profits rather than

wages. As I have argued before, there was a case for stronger

windfall profits on energy producers, and there remains a very strong

case for windfall profits on banks to offset the gains they are

making on holding reserves. However, none of this can avoid the fact

that wage inflation running at current levels in most of the private

sector is inconsistent with achieving the inflation target, which is

why interest rates have increased so much over the past year and a

half.

[3] There are a

whole host of reasons why wage inflation in the UK might be higher than

most models would predict, including data errors or backward rather

than forward looking inflation expectations.

[4] Food inflation

is still high however, and this will particularly impact those with

lower incomes, some of whom may experience further falls in their

real incomes.

[5] Because US

growth is much healthier than in the UK, as well as other reasons,

real wages have been rising for a year in the US.

{kind=link}