My investment philosophy is centered around buying quality dividend growth companies at an attractive valuation. I have discussed the importance of having a disciplined approach when it comes to prudent investing and avoiding overpaying for a stock.

Just like everything else however, valuation could turn out to be in the eyes of the beholder.

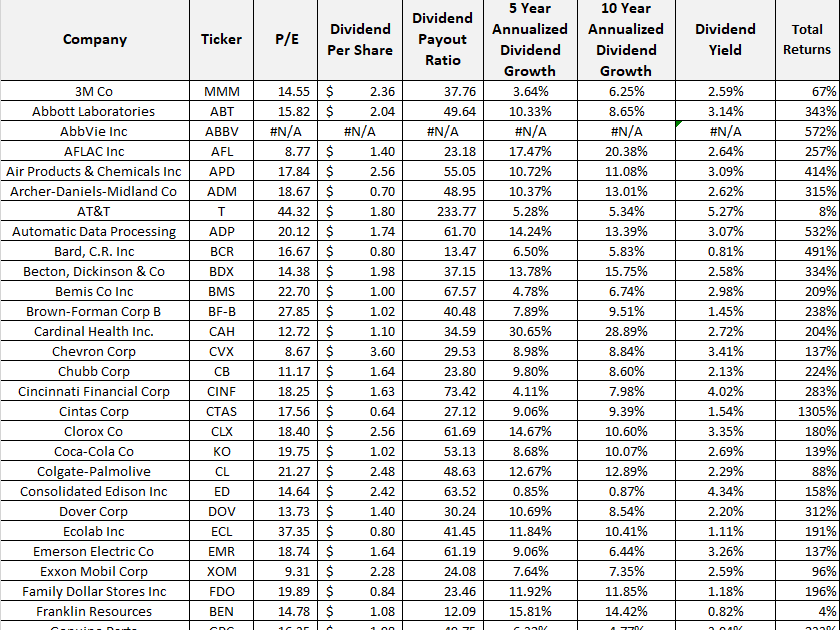

I was thinking about valuation, and its components “growth” and “value”, as I was compiling the returns of the Dividend Aristocrats from 2013. I looked at the ratios, and compared total returns through 2023 July 31.

Valuation is a double edged sword.

On one hand, if you overpay for a stock, you may end up losing money or not making much money.

On the other hand, if you’re too conservative on your valuation assessment and don’t invest, you may end up missing out on a lifechanging investment.

A stock may appear to be cheap, but in reality it could turn out to be a value trap as well. A primer example of that is AT&T over the past decade.

In my experience, I invested in Visa in 2011 when the stock was selling around 20 times earnings and had a dividend yield of about 0.70%. The stock seemed expensive at the time. Today it is up from $22 to $248/share and the dividend is at $1.80/share for an yield on cost of about 8%. In hindsight it seems cheap. If someone didn’t invest in it because the yield was too low, they would have missed out on an incredible compounding.

Another company that seemed cheaper was Con Edison. Stock sold at 16 times earnings and had a dividend yield of 4.10%. Stock seemed fairly valued at the time. Today, it is up from $59 to $90/share and the dividend is up to $3.24/share for an yield on cost of 5.50%.. In hindsight it does not seem as cheap, as its share price and dividend has barely kept up with inflation.

This discussion is more of a reminder that investing is part art, part science. It is not a scientific exercise like physics, that has known laws which can be applied at all times with the same result. There is always an unknown factor after all.

This is also a reminder to be flexible in ones approach, without being too lenient however. Valuation is taking into consideration both “value” and ‘growth” schools of thought, without looking at things in isolation. Per Warren Buffett, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive.

It’s definitely helpful to think through trade-offs, and opportunity sets, rather than thinking in definitive terms such as good and bad, black and white. It’s more of a gray.

When it comes to valuation, it is important to understand what drives future returns in a company.

In general, returns comprised of dividends and capital gains. The fundamental returns of a company are dependent on dividends and earnings growth. The speculative component is dependent on changes in the valuation multiple.

The US stock market has generated annualized returns of about 10%/year since 1926. This was driven by the 4% average annual dividend yield and the 6% growth in earnings per share. Any changes in the valuation multiple have had a very small impact over the past 97 years or so.

Changes in valuation multiples do not matter as much over really long periods of time. They do matter over shorter periods of time however, such as 10 or 20 years. This could be a long period of time for the average investor, who probably invests for the next 30 – 40 years.

I use this model in my investments as well.

In an ideal world, a company would grow earnings per share, grow dividends and increase intrinsic value at a decent pace over the course of time. Intrinsic value is the value of a business that could be attained by selling to another knowledgeable buyer. Think of a restaurant owner selling their business to another person. In an arms length transaction they are unlikely to just sell their blood, sweat and tears at a ridiculously low price, in relation to value. A reasonable buyer is also unlikely to massively overpay in an arms length transaction. That does happen in the stock market however.

In the real world, things are messier. For example, even if earnings per share and dividends per share increase at the same pace over a long period of time, the share price may not do so. That’s because share prices fluctuate much more than fundamentals, as observed by dividends and earnings per share.

As a result, share prices routinely may go above or below intrinsic value. This creates opportunities to buy shares of a good company at a discount. However, there are a lot of companies available at a discount or premiums to choose from. We need to compare not only one investment on its own merits, but also in relation to other investments. That’s our opportunity cost.

This works for comparing two companies. But in the real world, we also compare to other alternatives, such as investing in fixed income like US Treasury Bonds for example. Let’s simplify and just look at how I would compare two companies.

For example, a company that earns $4/share that never grows and pays $3/share in dividends may look cheap at $40/share. This company sells at 10 times earnings and yields 7.50%.

Another company that earns $4/share, grows at 10%/year and pays $2/share in dividends may look expensive at $80/share. This company sells at 20 times earnings and yields 2.50%.

Many retired investors may focus on chasing the high current yield of investment A, and ignore the smaller but growing dividend in company B. In my opinion, they should think about expected returns. They should also think about future yields on cost.

The expected returns on company A are 7.50%, assuming the earnings multiple stays constant. If you bought that stock and spent the dividends, after 30 years you would still be earning only 7.50% yield on the original cost. Chances are that those dividends would have a lower purchasing power due to inflation as well.

The expected returns on company B are 12.50%, assuming the earnings multiple stays constant. If you bought the stock and spent the dividends, after 30 years you would be sitting on an yield on cost of over 43%. Of course, just like chasing yield is bad, so is chasing growth. Trees don’t grow to the sky.

This exercise assumes that a high yielding company that never grows would be able to maintain that high payout ratio and that its business would go on without any changes for 30 years. That is a wild cart that may or may not turn out to be true. In reality, some companies with high payout ratios may end up cutting dividends if earnings per share hit a temporary slide. If the business starts descending into a permanent decline, those dividends may end up on the chopping block. We need to consider those trade-offs in the opportunity set.

This exercise also assumes that company B would have a high earnings growth for a very long period of time. That’s probable for a company with a strong moat, a competitive advantage of sorts, which has the pricing power and/or riding a long secular tailwind in demand to be able to grow earnings over a period of 30 years. Growth is never a given. If the business is unable to grow those earnings, valuation multiples would shrink. We need to consider those trade-offs in the opportunity set.

Of course, the same exercise will have different conclusions if valuations changed.

If company A above sold at the same multiple, but turned out they can grow at 2.50%/year, the expected returns goes up to 10%/year.

If company B above sold at a multiple of 40, and growth stayed at 10%/year, the expected returns go down. The yield would be 1.25% + growth of 10% would result in expected returns of 11.25%.

The same exercise will be even more fun as valuation multiples change

For example, if company A starts growing at 5%/year, then it may get re-rated from a P/E of 10 to a P/E of 15. That’s because it went from a period of low expectations to a period of unexpected good news. Investors who locked in an initial yield of 7.50% would also see some decent dividend growth and doubling of yield on cost in about 14 years. They achieve a high return because expected returns went from 7.50% to a higher amount. With a low P/E company however, the risk is that earnings are in a slow gradual decline. If they unexpectedly grow, that may be a good situation for the investor.

If company B however sees growth decelerating from 10%/year to 5%/year, then it may get re-rated from a P/E of 20 to a P/E of 10. That’s because it went from high expectations to lower expectations. Due to this re-rating of the stock, investors may sit for 14 years and see limited growth in the share price, even if earnings double over that time period. That’s because reality was worse than expected. Only return would be from the share price. The expected returns dropped from 12.50% to a lower amount.

That’s always one risk I think about with growthier dividend stocks – 1. That growth would decelerate 2 . That the P/E multiple may shrink as a result.

These scenarios were mostly a discussion of how I think about expected returns. They were discussions about how to calculate expected returns. They were also a discussion of the trade-offs involved and the possibility of potential outcomes that differ from expectations. It’s important to think about the risks and opportunities present, when making an investment. That can help position ourselves to better prepared to minimize the impact of any negative items thrown our way, while providing us with the opportunity to reap maximum rewards when the winds go our way.

After going through this exercise, along with my experience investing for the past few years, I’ve come to the conclusion that missing out on a potential big investment is a bigger sin than buying a bad investment. This of course assumes a diversified portfolio.

That’s because if you invest in a company, the most you can lose is the amount put to work there, minus any dividends received (unless reinvested through DRIP). But the amount that can be made is virtually unlimited. In other words, a potential great investment can pay for a few stinkers along the way, which the portfolio is guaranteed to have along the way.

In addition, it is hard to determine in advance, the conviction behind each investment. Hence, it may make sense to buy a diverse basket of quality companies, over time, with strong fundamentals, and then hold them. While it seems “irresponsible” to ignore valuation, in reality, it is hard to determine in advance if a stock is cheap or expensive. That’s because while we may know the P/E and dividend yield, we do not really know what the future EPS and DPS growth is going to be. At least that’s my conclusion from observing the aristocrats.

In practical terms, I view this as investing equally, in a group of companies that have qualitative characteristics (dividend growth companies). Then in the spirit of Coffee Can Portfolios, let the portfolio concentrate on its own, and rarely sell. It may be hard to try to avoid value traps (low P/E, low growth companies), and growth traps (high P/E, high expected growth). But that would be the cost of admission to end up with the quality dividend growth companies that grow earnings and dividends and intrinsic values for decades, building immense wealth in the process. That would more than compensate for any losers.

Going back to the main point of this article, valuation is a double edged sword.

If you overpay for a stock on one hand, you may end up losing money or not making much money.

If you’re too conservative on your valuation assessment and don’t invest on the other hand, you may end up missing out on a lifechanging investment.

A stock may appear to be cheap as well, but in reality it could turn out to be a value trap as well.

While it is not easy to “value”, you still need to take into consideration yield, growth, P/E ratios in order to make an educated guesstimate. You also need to be cognizant of trade-offs, and put yourself in the best position to benefit from any wealth creations from companies you invest in, while also minimizing losses as much as possible.

Relevant Articles: