US CPI Analysis

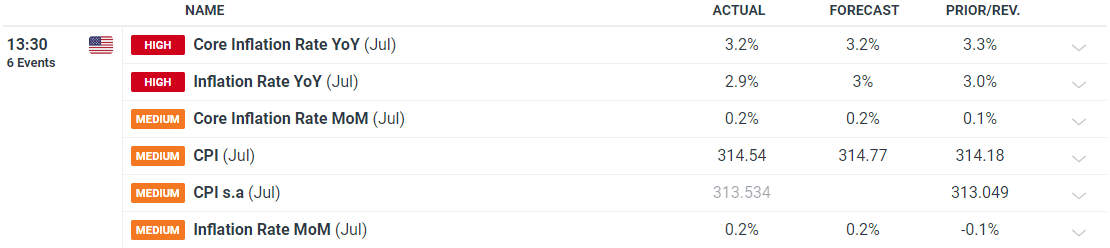

- US CPI prints mostly in line with estimates, yearly CPI better than expected

- Disinflation advances slowly but shows little signs of upward pressure

- Market pricing around future rate cuts eased slightly after the meeting

Recommended by Richard Snow

Get Your Free USD Forecast

US CPI Prints Mostly in Line with Expectations, Yearly CPI Better than Anticipated

US inflation remains in huge focus as the Fed gears up to cut interest rates in September. Most measures of inflation met expectations but the yearly measure of headline CPI dipped to 2.9% against the expectation of remaining unchanged at 3%.

Customize and filter live economic data via our DailyFX economic calendar

Market probabilities eased a tad after the meeting as concerns of a potential recession take hold. Softer survey data tends to act as a forward-looking gauge of the economy which has added to concerns that lower economic activity is behind the recent advances in inflation. The Fed’s GDPNow forecast foresees Q3 GDP growth of 2.9% (annual rate) placing the US economy more or less in line with Q2 growth – which suggests the economy is stable. Recent market calm and some Fed reassurance means the market is now split on weather the Fed will cut by 25 basis points or 50.

Implied Market Probabilities

Source: Refinitiv, prepared by Richard Snow

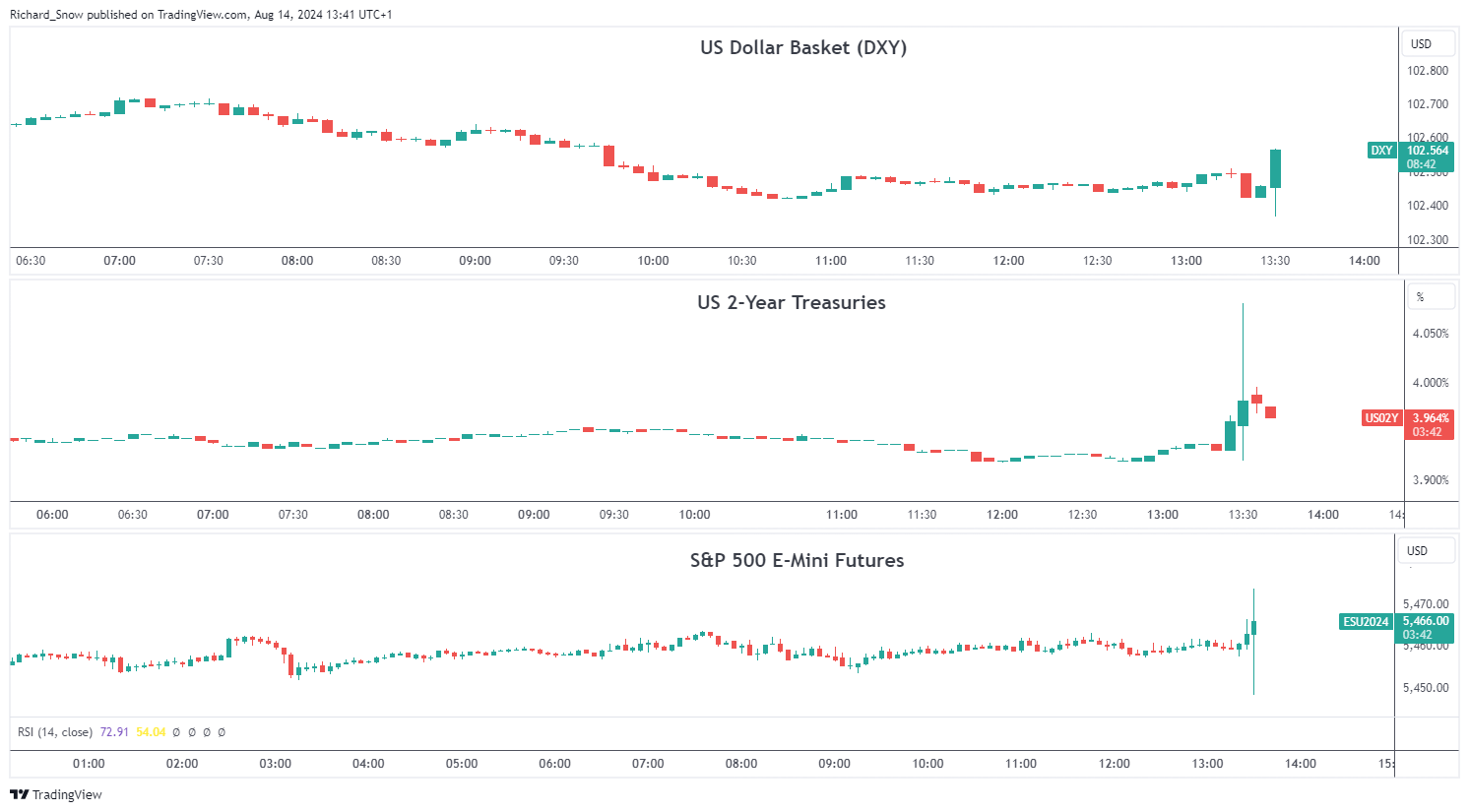

Immediate Market Reaction

The dollar and US Treasuries have not moved too sharply in all honestly which is to be expected given how closely inflation data matched estimates. It may seem counter-intuitive that the dollar and yields rose after positive (lower) inflation numbers but the market is slowly unwinding heavily bearish market sentiment after last week’s massively volatile Monday move. Softer incoming data could strengthen the argument that the Fed has kept policy too restrictive for too long and lead to further dollar depreciation. The longer-term outlook for the US dollar remains bearish ahead of he Feds rate cutting cycle.

US equity indices have already mounted a bullish response to the short-lived selloff inspired by a shift out of risky assets to satisfy the carry trade unwind after the Bank of Japan surprised markets with a larger than expected hike the last time the central bank met at the end of July. The S&P 500 has already filled in last Monday’s gap lower as market conditions appear to stabilise for the time being.

Multi-asset Reaction (DXY, US 2-year Treasury Yields and S&P 500 E-Mini Futures)

Source: TradingView, prepared by Richard Snow

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX

{kind=link}