Central banks worldwide – with the Fed and the ECB at the forefront – are on the brink of implementing their historically rapid policy reversal, yet interest rates are already setting new records on a daily basis. And there’s not much chance of this changing any time soon.

To make things tangible: The German 10-year rate has dropped to almost -0.40{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}. That means that the foundation upon which almost all rates in the Eurozone are based, is negative. In Japan, where the 10-year rate is at -0.16{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}, the same applies. In Switzerland the yield curve only offers you negative yields, hence everywhere between a maturity of 3 months and 50 years.

Bare bones

For those looking to earn even a little bit more, risk-taking is the name of the game. If you lend your money to the Austrian government for the extremely long maturity of 100 years, then you’ll get 1.04{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} in interest each year – a rather pitiful amount. If you’re comfortable lending to Italy, then you can count on 1.47{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} per year for a period of 10 years, and 2.76{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} for a maturity of 50 years.

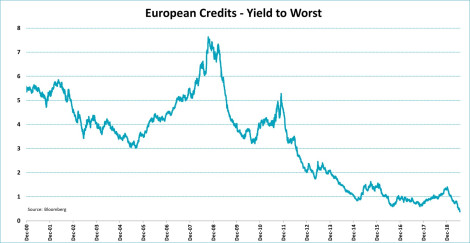

For that you get a debt ratio of 133{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} of GDP, a structural budget deficit and as good as zero percent economic growth in return. And for those imagining that the rewards from lending to corporates are better, forget it. Over a diversified basket of European corporate debt with a high degree of creditworthiness, you’ll barely earn 0.40{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} in interest. Another unimpressive return.

Only in the US – where the central bank has been so bold as to reverse some of its previous, abnormal policy – are rates just a little higher without having to face enormous risks. But that’s about to end too. Fed Chair Powell will lower rates as soon as next week, with only some uncertainty on how much (25 bps or 50bps).

Back to normal?

In anticipation of this, interest rate levels have tanked in the US as well. The 10-year rate is still just a tad over 2{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}, while just nine months ago you would earn 3.25{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}. The chance of a rapid return to normal rate levels – and by normal I mean at least a fair compensation for the risk you’re willing to take for lending your money – is extremely unlikely.

Although many central banks have already announced the major reversal in their policy, they have yet to implement it. The ECB could cut rates today, or at least hint at a rate cut in September. It could also signal it’s considering a fresh round of quantitative easing. Where the Fed is concerned, one rate cut let it be 25 bps or 50 bps, the first rate cut is almost always followed by more.

Central banks are stubbornly sticking to the policy of making money cheaper (read: forcing interest rates downwards) to achieve their ultimate goal – often an inflation level somewhere around 2{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}. Although central bankers talk convincingly about the number of instruments in their toolbox, all those instruments basically do the same thing. And that despite the fact that the world really is a different place now.

A losing battle

Services, especially technology-driven services, represent a growing share of the economy. Technological developments have the appealing benefit that they often make things cheaper. Stimulating the economy with lower interest rates might be great for manufacturing industries, which require large capital injections, but technology often does not need such large investments.

It sometimes seems like central banks are fighting a losing battle. And as long as they refuse to adapt their strategy, a loss is almost a given. So for the time being, just expect more of the same – which means positive rates will remain scarce.

*This blog was derived from the ‘Chart of the Week’ on the Robeco website

https://www.robeco.com/en/insights/graph-of-the-week.html

SOURCE: Jeroen Blokland Financial Markets Blog – Read entire story here.