Dividend stocks (WMB, KMI, IIPR) will rally once the rate cuts begin. We are getting so close, and I think September is iffy for a cut, but if this trend continues, October would be a lock.

“Davidson” submits:

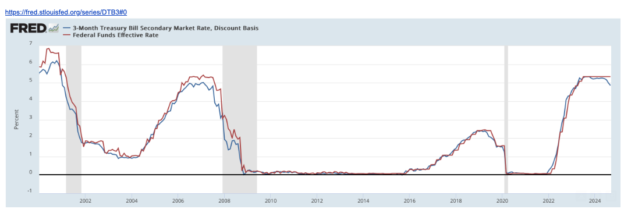

T-Bill Secondary Mkt on Discount Basis appears to be the Fed Funds benchmark. It is this T-Bill rate which moves 1st that Fed Funds follows in a few weeks always keeping a premium. At 4.85% today, the spread between the T-Bill and Fed Funds is enough to permit the Fed to cut but too early to do so as it usually needs to see T-Bill rates stabilize at the new level for a couple of weeks before acting.

However, EU Central Bankers have already moved despite much higher inflation, and this pressures Powell into moving faster than he may have anticipated. He may cut shortly or wait till Oct when he is surer of the direction of T-Bill rates.

Institutional money now sees the 30yr minus 2yr indicator as having turned economically bullish with some adjustments already made strategically away from only favoring Mag 7 issues. It seems likely that both T-Bills out to 2yr Treasuries may have been shorted against longer dated Treasuries to benefit from a rate decline. Seeing the 30yr minus 2yr turn positive first because there was more risk in being short the 2yr vs short T-Bills makes sense. This is a market psychology process with many along the perspective-spectrum. Some have reacted and adjusted causing the Mag 7 to stall. Others will react as they sense their conviction wane, but the shift is apparent and likely to continue.