Six years ago, on March 09, we hit the low in stock markets. After five quarters of falling stock prices, the S&P 500 index hit 666 (yes 666), the bottom was finally reached. What followed was one of the biggest stock market rallies of all time, which, by the way, has not officially ended yet. The historical rally of the last six years was largely powered by one very powerful force. Unmistakably that of central banks!

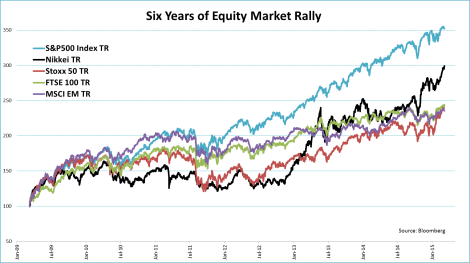

Equities

The chart below shows that, during the last six years, the S&P 500 index gained a mind-boggling 250{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}, or an average of 23{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} per year. But other equity markets recorded big returns as well. Emerging markets, which are the ‘laggard’ of this rally so far, still managed to realize an average return of 15{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} per year, to reach a six-year total of 135{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}. Not too bad I would say.

Bonds

But equity markets were not the only markets that rallied. Bond markets, especially those in the Eurozone and the UK, realized some big returns as well. Eurozone government bonds rose 42{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} during the last six years, most of which came in recent years as the ECB ultimately gave in and started its own QE program. And this is just the Eurozone average. For instance, Portuguese government bonds have returned more than 60{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} in the last six years. But even in the US, where bond yields were already relatively low in March ’09 and have not shown the dramatic decline like in the Eurozone, the return averaged 3.2{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6} per year.

Yields

Unlike in the US, bond yields in the Eurozone and Japan fell to zero or even below. Low inflation and slow growth surely had a downward effect on rates, but the extraordinary measures by first the BoJ, and later the ECB, really pushed bond yields down to incomprehensible levels. The graph below only shows the 10-year yields, but many of the (short-term) yields are negative and falling. German bond yields are negative up to 7 years! In fact the only region where rates did not come down is emerging countries. Many central banks in emerging countries could not or didn’t have to go to extremes.

Central Bank Rates

That most countries in developed countries did go to extremes is neatly illustrated by central bank rates. In the last six years they have been extremely low, and in some cases, like Switzerland, even negative. Not just a little by the way, the current SNB rate stands at -0.75{01de1f41f0433b1b992b12aafb3b1fe281a5c9ee7cd5232385403e933e277ce6}. Another thing that six years of central bank dominance proved: zero is definitely not the lower boundary.

Balance Sheets

Central bank balance sheets are perhaps an even better illustration of the biggest real-time financial experiment ever conducted. Central bank balance sheets have exploded as already low interest rates led them straight into the liquidity trap. The ECB was the only dissonant for a while, but as mentioned it joined the experiment a while later. As (real) rates were not negative enough to get things going again, central banks decided to help the markets a ‘little’, blowing up their balance sheets on the way.

Inflation

One possible outcome of the experiment, a massive surge in inflation levels, has not occurred, yet. If anything inflation levels have come down. This made some central banks, like the Bank of Japan, to blow up their balance sheets even more as their main goal is maintaining an adequate level of inflation. But victory can’t be claimed at this point in time. They did succeed in one thing, though. The massive liquidity experiment has made everything rally in the last six years, from equities to bonds. I wonder what the next six years will bring.

Filed under: BONDS, EQUITIES, FINANCIAL MARKETS Tagged: Bonds, central banks, Equities, Inflation, market rally, QE, yields

![]()

SOURCE: Jeroen Blokland Financial Markets Blog – Read entire story here.