It is usually quite hard to spot a new trend and then work on finding stocks (listed) that fit the criteria. There are a number of reasons for it, the greediest, smartest, shrewdest poker players in town (private equity) would not let such a listed company be public. A few examples of up coming trends are use of Graphene as the silicon of 21st century, Battery storage technology for solar grids, Robotics (humanoids or systems with AI).

We do get lucky once in a while by spotting companies that are not on the map, or those that have changed their business model.

If you recall from some of my previous posts, products that help women look pretty, or allow humans a longer life, or deceptively even a perception of being healthy (eg: perception of healthy Patanjali Food stuff, even though it may contain three times the pesticide content of Maggi) are perpetual models (nice book on business models http://tinyurl.com/pe7lu2m) to be exploited by capitalists. I hate exploitation or taking advantage of others based on psychological tricks or diplomacy (Nice book on how not to get duped by other marketers from Cialdini http://tinyurl.com/ol4xpql).

Nevertheless, I am not blind to the fact what is going on in the Advertisement industry and social media or the world around me. Organic *everything* is on an upward trend or at-least I am a sucker for it by paying 2.5x the non-organic food.

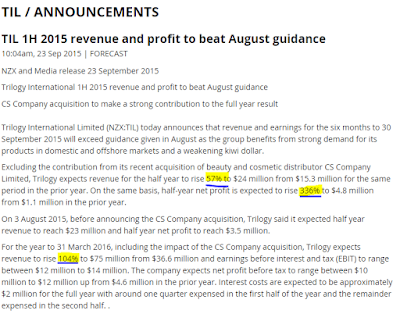

I just happened to stumble on an announcement recently from a company based in New Zealand that it will beat organic growth target of 57% growth (excluding acquisitions).

Source: https://www.nzx.com/companies/TIL/announcements/270582

I had been searching all over for organic food companies like a musk deer, the company that I should have bought was right near my back(yard) literally.

The story gets better as the company went in for a bolt-on acquisition funded entirely by debt of another strong company that imports Gucci, LVMH, Aramani and other perfume brands in New Zealand. But excluding the growth of acquired company the organic growth is 57% in revenues.

I checked and found that I am indeed late to the party with stock up 300% or so recently.

The company had been struggling to create a cosmetic brand called ECOYA

http://www.ecoya.com/

The company has a second brand now Trilogy

http://www.trilogyproducts.com/

Some fortunate events transpired in the life of this company, Kate Middleton and few Supermodels in Europe provided free publicity to Trilogy, the recently introduced product “ORGANIC Rose Hip Oil”. Certainly a formula that is good for supermodels and the Royalty is also good for the gentry and lower classes.And you certainly cannot pay princess to be a brand ambassador for your product.

Reference: http://www.dailymail.co.uk/femail/article-2986045/Is-rosehip-oil-secret-Duchess-Cambridge-s-pregnancy-glow-Royal-said-fan-natural-oil-keeps-wrinkles-bay-s-sold-out.html

http://www.express.co.uk/life-style/style/562964/Kate-Middleton-pregnant-wrinkles-rosehip-oil-Carole-Middleton

https://www.google.co.nz/search?q=kate+middleton+rosehip

http://www.trilogyproducts.com/trilogy-talk/royal-seal-of-approval/

Organic products such as Trilogy beauty products are also “pregnancy safe”, and boy you gotta see the salivating margins on these products for infants and pregnant women.

It gets better, did I say, even better !

The company has signed up with most respected Organic chain in the US. It has introduced product in the US in every store of Whole Foods Mart the Organic Supermart. Currently the revenues in Australia account for 50% of sales, NZ 25% and US only 5%, ROW 20%. US revenues are now growing 100%+

I know the question comes to mind about valuations, extremely inexpensive at 14 times earnings 1 year forward. 1 time sales. In rest of the globe, in developed countries FMCG companies are trading at 3-10 times revenues and 30-80 times earnings, and they are not growing this fast. The company has broken out of 20% growth trajectory and now in 30-40% orbit, this year 60% actually.

I avoid developed markets for investment, too many eyeballs, too much capital chasing at too laggardly growing companies. This is only the one out of two companies I like in New Zealand for investment. Last time in 2013 I liked a company in Australia, CAPILANO Honey and read in their annual report “We are quite satisfied with 10-12% growth”, hence gave a pass.

I wrote about this company as “The only company I like in Australia” two years back http://multibaggersindia.blogspot.com/2013/09/roe.html

Capilano went up nearly 10 times, 1000%, even now at in-expensive 18 times earnings.

How much up a stock has gone up on the past has nothing to do with how much it will go in future. I bought Symphony in 2010 at 25 Rs when it had already gone up 10 times from 2.5 Rs. It went up another 100 times from that point.

Not letting go of this opportunity which I think will grow well above 15%, and approved by the Royalty!

Link to Annual Reports: http://trilogyproducts.com/investors/

{kind=link}