Updated with M1 Plus price drop and lots of promos. New $250 referral and 401k rollover bonus. I’ve tried out my share of robo-advisors, which always sounded nice in theory but I eventually became disillusioned as they kept generating lot of unnecessary taxes every time they change their model portfolios to chase the latest and hottest trends. My favorite service for those that want a little extra help is one where I can pick my own custom target portfolio, but the robo still does the hard work: M1 Finance. Here’s a quick rundown of what makes them different:

- Fully customizable. You pick your own target asset allocation “pie”. (You can add ETFs or individual stocks.) You can simply copy one of the many model portfolios out there, or make your own custom pie as you like. You have full control! M1 handles the tedious stuff, like rebalancing or dividing a $100 contribution across 8 different ETFs.

- No commissions. Free stock/ETF trades with a low $100 initial minimum for taxable accounts and a $500 minimum opening amount for retirement accounts. After your initial deposit any amount greater than $10 can be deposited.

- 0.00% management fee! Most robo-advisors charge an annual management fee of 0.25% to 0.50% of assets, or force you to own something bad, like a lot of low-interest cash. (Looking at you, Schwab…)

- Free dynamic rebalancing. All new deposits (and withdrawals) will be invested (or sold) dynamically to bring your portfolio back toward your target asset allocation. M1 will also rebalance your entire portfolio back to the target allocation for you with a few clicks (for free) whenever you choose, on demand. You don’t need to do any math or maintain any spreadsheets.

- Fractional shares (dollar-based). For example, you can just set it to automatically invest $100 a month, and your full amount will be spread across multiple ETFs. Dollar-based transactions were one of the advantages of buying a mutual fund, but fractional shares solve this problem. ETFs are also usually more tax-efficient than mutual funds.

- Real brokerage account with off-the-shelf investments that you can move out. Some robo-advisors hold special, proprietary funds that you have to sell if you ever leave, possibly creating a big tax bill. (Looking at you, Fidelity…) M1 is built on a regular brokerage account, so you can move your Vanguard/iShares/Schwab ETFs and stock shares out to another broker whenever you want.

M1 Finance checks off nearly all the boxes of my brokerage wish list. I suppose the only thing they could add would be to have the high availability of knowledgeable customer service of a huge company like Fidelity or Schwab. Otherwise, I really like their feature set and I have been putting my recent annual IRA contributions into M1.

If you want to invest in newer factor ETFs that focus on Small-Cap, Value, Momentum, or Quality factors like those from DFA and Avantis, or a mix of dividend-oriented ETFs like SCHD/VIG/VYM, their service makes it much easier to set up a portfolio mix of different ETFs.

M1 Plus. M1 Plus is their premium subscription tier with several additional perks, and the price has dropped to $3 a month ($36/year). This is a significant drop from their old pricing of $10/month or $95/year.

- High-yield savings (currently 5.00% APY as of 1/10/24). FDIC-insured up to $5 million.

- M1 Owner’s Rewards credit card (2.5%, 5%, or 10% cash back at 70+ brands, no annual fee).

- Lower interest rates on margin borrowing (1.5% rate discount).

- Custodial accounts for kids.

- Extra 3pm PM ET trade window.

- Automated “smart” transfers.

Personally, there is no “gotta have” item here for my purposes, so I don’t have M1 plus on my accounts, but the high-yield savings account is nice if you want to keep your life simple and you hold a decent amount of cash. The pricing is also more reasonable now.

$250 referral bonus. M1 has boosted their referral bonus way up to $250 if you open a new account with $10,000 and maintain it for 30 days. You’ll also get 6 months free of their M1 Plus premium service. Here are the $250 bonus details (the current promo which expires March 31, 2024). Here is my M1 referral link (thanks if you use it!) from which you must start opening your new account.

A bonus that amounts to 2.5% of your initial deposit with only a 30 day hold is technically a 30% annualized yield. This is also over 3x better than their standard offer for a $10,000 new deposit (see below), and you can also consider the ACAT transfer and retirement rollover promos below.

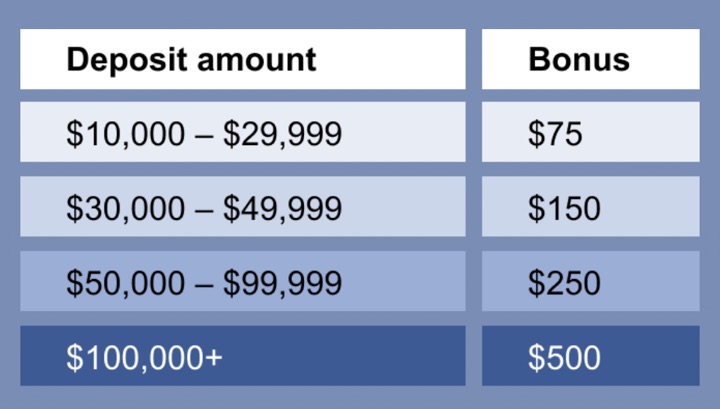

Up to $500 New User deposit bonus. Deposit $10,000 or more within two weeks of opening your new M1 Brokerage Account and get a cash bonus of $75 – $500 deposited to that account. See deposit bonus promotion link for full details.

Up to $20,000 ACAT Transfer bonus. You can get up to $20,000 when you

transfer brokerage assets via ACAT to M1 by 3/31/2024. See ACAT transer promotion link for full details.

Up to $5,000 Retirement Rollover bonus. You can get up to $5,000 when you

roll over your 401(k), 403(b) or another employer-sponsored retirement plan in an M1 Traditional/Roth IRA account by 3/31/2024. See this Retirement rollover promotion link for full details.

Bottom line. M1 Finance is a brokerage account that acts like a free, customizable robo-advisor with automatic rebalancing into a target portfolio. You control the model portfolio, and they do the tedious work. Great for implementation of a low-cost, index or passive ETF portfolio.

Disclosure: I am now an affiliate of M1 Finance, and may be compensated if you click through my link and open a new account.

Also see: Big List of Free Stocks For New Commission-Free Brokerage Apps