The market was disappointed yesterday, to say the least!

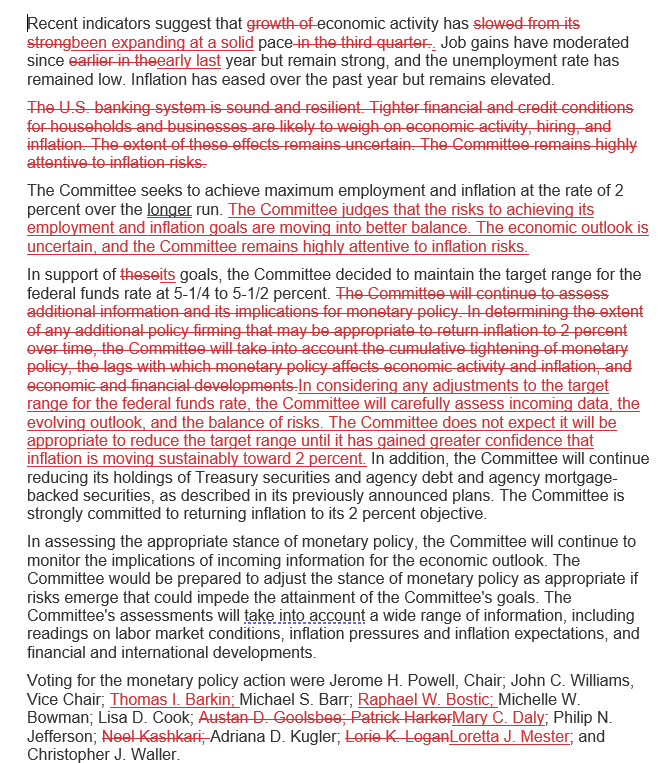

Yesterday’s more hawkish Fed comments paint a picture of a Fed that’s not just holding the line but actively pushing back against market expectations. The FOMC unanimously voted to keep rates steady, with a clear message: no rate cuts until there’s greater confidence in inflation moving sustainably towards 2 percent and we just had our CPI Report and it looked like this:

The Fed’s statement was a master class in saying a lot without saying much at all. They’ve removed references to “tighter financial conditions” and “growth slowing,” which is like saying, “Everything is fine, but don’t quote us on that.” The most intriguing part? The omission of the usual “U.S. banking system is sound and resilient” comment. It’s like removing “I’m fine” from a teenager’s vocabulary – it speaks volumes.

So, what does this all mean for the future landscape of rates in 2024? The Fed is playing a long game. They’re not just looking at current economic indicators; they’re peering into their crystal balls, trying to predict where the economy will be months, even years, down the line. The Fed’s latest move is a juggling act of maintaining economic stability, managing inflation expectations, and navigating the choppy waters of election-year politics. For investors and market watchers, it’s a signal to buckle up – 2024 is going to be an interesting ride. And as for rate cuts? Don’t hold your breath…

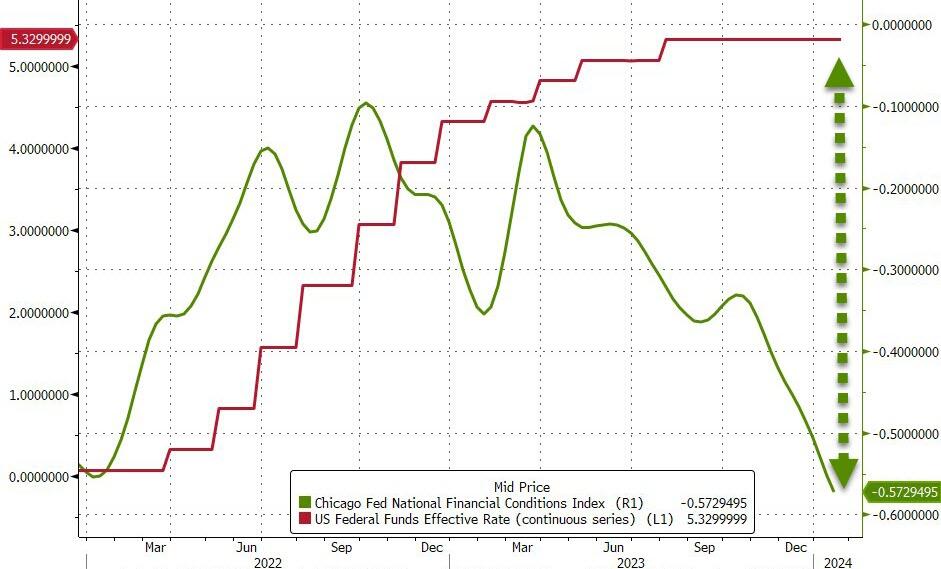

The NFCI aims to give a comprehensive weekly overview of U.S. Financial Conditions, covering aspects like money markets, debt and equity markets, and both traditional and “shadow” banking systems. It includes three categories of financial indicators: Risk, Credit, and Leverage. The NFCI is constructed to have an average value of zero and a standard deviation of one over a sample period extending back to 1971. Positive values indicate tighter-than-average financial conditions, while negative values indicate looser-than-average conditions.

As you can see from the chart, it’s taken this long just to get financial conditions back to normal and yes, higher rates make lenders happier to loan money so of course conditions are now “looser” and this is all part of the Fed’s plan to engineer a “soft landing” and, so far – it looks like it’s working, with the index implying easier access to credit, lower risk premiums, and generally more accommodative financial conditions.

HOWEVER – Looser financial conditions can also contribute to higher inflation. Easier credit and lower borrowing costs can increase demand in the economy, potentially pushing prices up, especially if the economy is near or at full employment, as ours is. The Fed is rightly aiming to “watch and wait” – no matter how impatient investors and politicians are getting.

HOWEVER – Looser financial conditions can also contribute to higher inflation. Easier credit and lower borrowing costs can increase demand in the economy, potentially pushing prices up, especially if the economy is near or at full employment, as ours is. The Fed is rightly aiming to “watch and wait” – no matter how impatient investors and politicians are getting.

IN PROGRESS

Related posts:

New Orders & Retail Sales Motor Vehicle & Parts vs Lt Weight Vehicle SAAR and the Manheim Index All Positive – ValuePlays

New Orders & Retail Sales Motor Vehicle & Parts vs Lt Weight Vehicle SAAR and the Manheim Index All Positive – ValuePlays

End of the Month Summary – March 2015

End of the Month Summary – March 2015

Bitcoin Ecosystem Set For Remarkable Growth In 2024: Research Projects 1,200% Growth In These Projects

Bitcoin Ecosystem Set For Remarkable Growth In 2024: Research Projects 1,200% Growth In These Projects

US oil production forecast to reach new heights despite drilling slowdown

US oil production forecast to reach new heights despite drilling slowdown