“Davidson” submits:

Industrial Production reported a positive surprise. However, several analysts have announced the beginning of the ‘next recession’ in a 2yr series of such announcements based on the PMI and other factors such as the dramatic inversion in the Yield Curve. Nonetheless, Real Retail Sales and Industrial Production do not concur. Real Retail Sales are holding at an elevated level very likely due to consumers being forced to abandon the many small retailers not reported. The loss of these retailer’s unreported sales has suddenly shown up in those businesses who do report. This makes it difficult to compare current vs past retail sales data. The best that can be said is that retail sales are holding up and not indicating weakness associated with a pending recession. Industrial Production continues to move sideways at a level similar to prior peaks. That the manufacturing PMI has forecasted recessions roughly 3x greater frequency than those that occurred indicates that the PMI represents market sentiment, not economics. The equity markets are currently responding to recession fears and hitting new highs by an absurd amount of capital crowding into the top 10 issues. Nvidia(NVDA) is currently priced 41x Pr/Sales with other issues routinely 10x+ and without any particular change in its growth prospect, Eli Lilly(LLY) is priced at 21x+. Meanwhile, there has been a dramatic surge in industrial earnings and year-ahead-guidance that are mostly ignored and remain well below historical Pr/Sales.

At some point, investors will rediscover the latter. Markets dip with the PMI under 50 and are decent buying opportunities especially when economic indicators do not agree. There continues to be no recession ins sight even with continued forecasts that a recession has already begun.

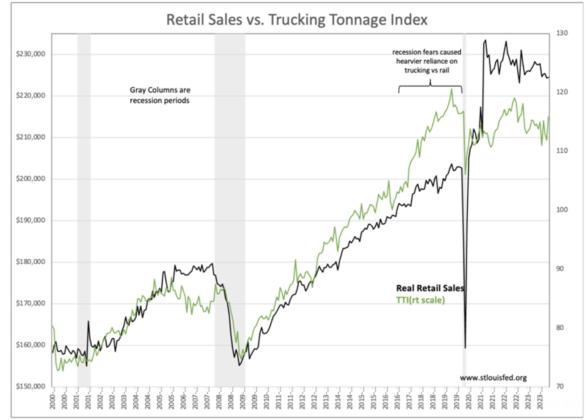

Now, all the above is true, but we also have to look at hard indicators, like tuck tonnage and retail sales, which continue to meander sideways, albeit at elevated levels. This continues to cause me to remain cautious.