“Davidson” submits:

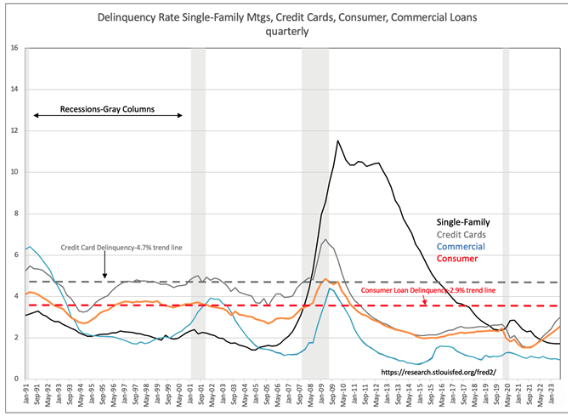

Once a quarter, the St Louis Fed releases delinquency rates on consumer and business loans. With the consumer 67.8% of GDP this chart shows the two categories of consumer borrowings, Single-Family Mortgages and Consumer Loans with a sub-set of Credit Card debt. Commercial Loans represent the business borrowings. Excepting the COVID shutdown in 2020, a non-economic event, every recession was preceded by high consumer delinquency rates representing a pre-recession financial stress during which consumers were unable to pay back borrowings. In each instance an unexpected event caused banks to slow lending and as delinquencies turned into defaults the US economy tumbled into recession. Consumer delinquency rates for credit cards at the 4.7% and consumer loans at 2.9% are dangerous financial stress points. Current delinquency rates remain well below these levels and are even below periods of prior economic growth. Not only is there little financial stress in our economy. It is likely to take 2yrs-3yrs before we reach those worrisome levels.

Those who continue to call for recession and speak of rising consumer debt are missing the fact it is the consumer’s ability to handle that debt not the level itself that is the key economic element. Thus far, all is good. Many equities reflect a recession fear that has not been rewarded. Companies core to the US economy have been reporting business as usual with record revenue, record profits and higher guidance quarter by quarter since recession fears began 2 years ago, Dec 2021. Employment and retail sales have risen. Construction spending, durable goods orders have been soaring. These are signs of robust economic activity as reflected in US GDP. GDP and Real GDP do not turn down on a proverbial “dime”. If one looks, each represents acceleration back to the pre-COVID prior trend shown for Real GDP.

Buy equities of companies representing core US economic activity.