BoE, GBP, FTSE 100, and Gilts Analysed

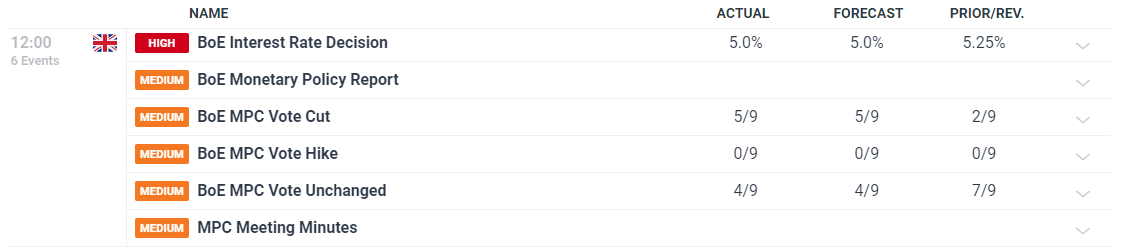

- BoE voted 5-4 to lower the bank rate from 5.25% to 5%

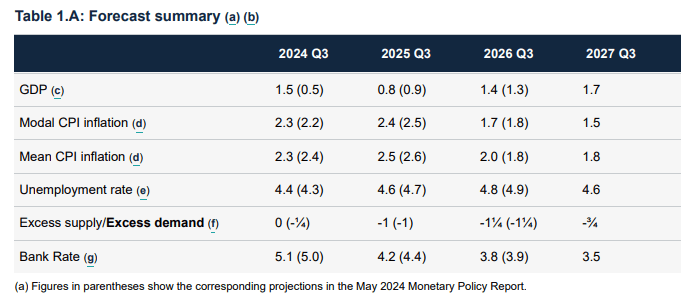

- Updated quarterly forecasts show sharp but unsustained rise in GDP, rising unemployment, and CPI in excess of 2% for next two years

- BoE cautions that it will not cut too much or too often, policy to remain restrictive

Recommended by Richard Snow

Get Your Free GBP Forecast

Bank of England Votes to Lower Interest Rates

The Bank of England (BoE) voted 5-4 in favour of a rate cut. It has been communicated that those on the Monetary Policy Committee (MPC) who voted in favour of a cut summed up the decision as “finely balanced”.

In the lead up to the vote, markets had priced in a 60% chance of a 25-basis point cut, suggesting that not only would the ECB move before the Fed but there was a chance the BoE could do so too.

Lingering concerns over services inflation remain and the Bank cautioned that it is strongly assessing the likelihood of second-round effects in its medium-term assessment of the inflationary outlook. Previous reductions in energy costs will make their way out of upcoming inflation calculations, which is likely to maintain CPI above 2% going forward.

Customize and filter live economic data via our DailyFX economic calendar

The updated Monetary Policy Report revealed a sharp but unsustained recovery in GDP, inflation more or less around prior estimates and a slower rise in unemployment than projected in the May forecast.

Source: BoE Monetary Policy Report Q3 2024

The Bank of England made mention of the progress towards the 2% inflation target by stating, ‘Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further’. Previously, the same line made no acknowledgement of progress on inflation. Markets anticipate another cut by the November meeting with a strong chance of a third by year end.

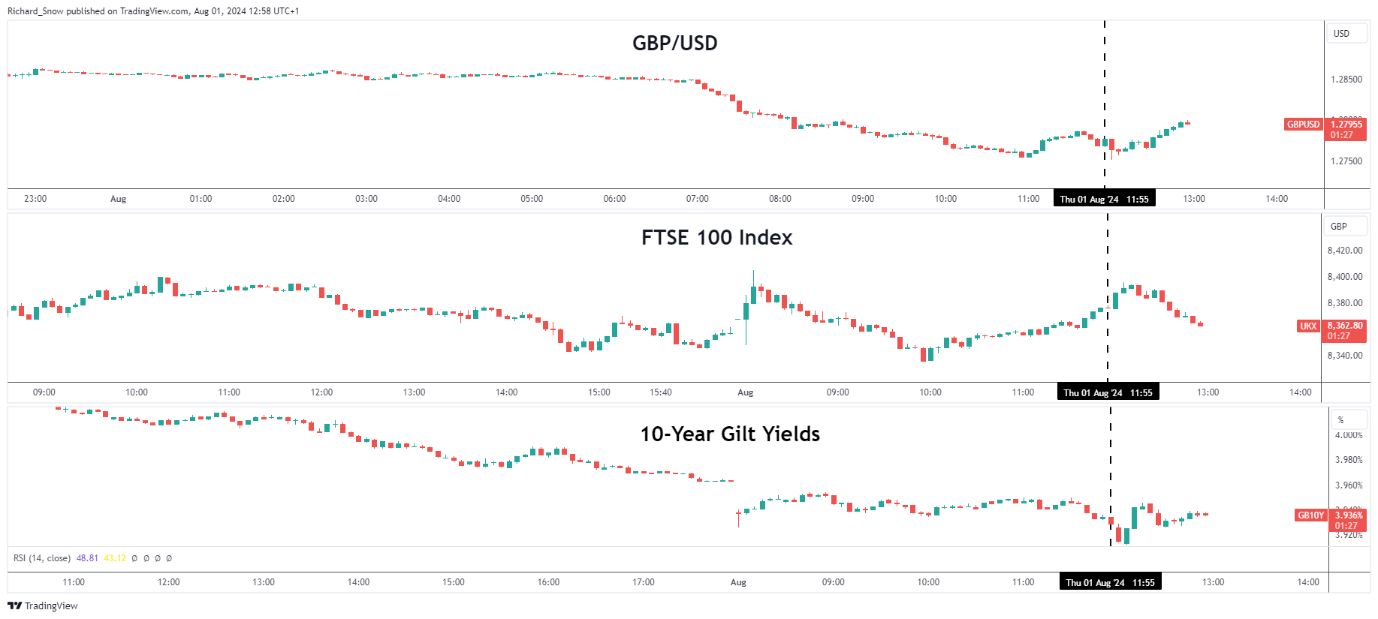

Immediate Market Reaction (GBP, FTSE 100, Gilts)

In the FX market, sterling has experienced a notable correction against its peers in July, most notably against the yen, franc and US dollar. The fact that 40% of the market anticipated a hold at today’s meeting means there may be some room for a bearish continuation but it would seem as if a lot of the current move has already been priced in. Nevertheless, sterling remains vulnerable to further downside. The FTSE 100 index showed little response to the announcement and has largely taken its cue from major US indices over the last few trading sessions.

UK bond yields (Gilts) dropped initially but then recovered to trade around similar levels witnessed prior to the announcement. The majority of the move lower already took place before the rate decision. UK yields have led the charge lower, with sterling lagging behind somewhat. As such, the bearish sterling move has room to extend.

Record net-long positioning via the CFTC’s Cot report also means that massive bullish positions in sterling could come off at a fairly sharp rate after the rate cut, adding to the bearish momentum.

Multi-Assets (5-min chart): GBP/USD, FTSE 100, 10-year Gilt Yield

Source: TradingView, prepared by Richard Snow

| Change in | Longs | Shorts | OI |

| Daily | 5% | -12% | -5% |

| Weekly | 16% | -23% | -9% |

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX

{kind=link}