As a dividend growth investor, I invest with the end goal in mind.

My goal, from the very beginning of my journey, has been to generate a certain amount of target dividend income per year. Dividend income is more stable, reliable and easier to forecast than share prices. That’s because share prices are much more volatile than dividends. Dividends are correlated with company cashflows in the short-run and long-runs, and those cashflows are much less volatile than Mr. Market’s opinion of the value of those cashflows. Dividends are the only direct link between a company’s financial performance and the investor.

Share prices on the other hand represent the collective opinion of market participants, who may bid prices above any reasonable estimate of intrinsic value if they are excited about the company OR sell them off below any reasonable estimate of intrinsic value if they are gloomy about the company. Share prices tend to fluctuate much more than company cashflows. This is why even a well known company like Apple can sell at a wide range of valuation multiples, like 15 to 35 times earnings, over the course of an year.

It’s much easier to forecast the dividend that a company would pay in a given year, than the share price at which it would sell over the course of a given year. For example, for a company like Apple computer, it is much easier to forecast that it would pay at least $1/share in dividends. But it’s impossible to tell if the stock price would go above $230 or below $130.

Those share price fluctuations don’t matter as much in the accumulation phase. However, this really matters when you get closer to your estimated retirement date and even more important when one is retired. That’s because if you have to sell shares to fund your lifestyle, you are now exposing yourself to short-term price fluctuations. You are essentially betting that your portfolio will generate enough gains in the short term, year in and year out, so that you do not run out of money in retirement. You are also exposed to fluctuations, and sequence of returns risk. This basically means that your retirement outcomes will be greatly influenced if you have to sell stock when prices are low, to their potential detriment. If you are lucky, and share prices only go up however, it would be smooth sailing for you.

To paraphrase the movie “Dirty Harry”, Are you feeling lucky, punk?

If I have a diversified portfolio that generates $60,000 in annual dividend income per year, I can be reasonably certain that I would generate at least that much in the next few years. It’s very likely that this portflio would generate dividend income that grows above the rate of inflation actually. That portfolio would likely have to be invested in blue chip dividend growth companies, in the dividend aristocrats, dividend champions, dividend achievers types.

If the investor needs $60,000 in annual dividend income in retirement, they are set for life. Getting there is simple, and is the end result of how much you invest, what returns you generate (dividend yield + dividend growth) and how long you invest for. For each $1,000 that you invest, you are essentially buying income. In general, depending on the yield/growth trade-off you are willing to make, you can generate probably $20 in a higher dividend growth/but lower dividend yield portfolio. Or you can generate say $30 in a medium yield/medium growth portfolio tilt. I wouldn’t chase yield at this time, but it is also possible to generate $40 in a higher yield but lower growth portfolio. For the purposes of this exercise, let’s assume that you can generate $30 in dividends for each $1,000 you invest.

In the accumulation phase, that dividend income gets reinvested, and those dividends increase. You also keep buying more future income, and you build that portfolio out, brick by brick.

That dividend income keeps growing, slowly at first, and then the snowball really accelerates. The neat thing about that total dividend income is that it is more stable than prices. So that dividend income keeps marching forward, year in, and year out, assuming of course diversified portfolio that is not concentrated in a single sector or two. Or even worse, concentrated in less than 20 companies. So it is important to be diversified, holding a lot of individual dividend growth companies, representative of as many sectors that make sense at the right entry price.Then to hold.

The neat thing about US dividends is that they rarely decrease. At least in the past 80 years or so, dividend income has rarely decreased for diversified US portfolios. The only exception was in 2008, when the US economy was on its knees, during the Global Financial Crisis. Even then, when those dividends fell by 20% top to bottom from 2007 to 2009, share prices fell by 60%.

So you can easily see the projected dividend rise, until it reaches the dividend crossover point. That’s the point at which dividends pay your expenses. Since dividends are more stable and predictable than share prices, you know exactly where you are on your journey, during your journey. You also know exactly when you can retire. So if you retire when you reach your dividend crossover point, you are more certain that you would receive your target dividend income from your diversified dividend portfolio. Than if you were to rely on forecasting prices and selling at the right price.

On the other hand, that portfolio could be valued at any range at the marketplace. If could be priced at say $3 Million in a bull market (2% yield) or could be worth say $1.50 Million in a bear market (4% yield).

If you were reliant on share prices, you may be in for a little bit of a surprise. For example, assume you owned a portfolio and planned on selling shares to fund your lifestyle. You plan to sell 3% of your initial portfolio value, and then sell enough stock to pay expenses and increase that by rate of inflation.

That’s all fine and dandy, but now you are reliant on short-term share price fluctuations for your retirement.

Of course, most people today are told that the 4% rule is safe. The 4% rule basically states that you determine how much money you have, and then you can sell an amount equal to 4% of the initial portfolio value, and also increase that with inflation. So if you retired with $1 Million in 1999, you plan to spend $40,000 in 2000, and a little more than $40,000 in 2001 (by adding inflation), etc.

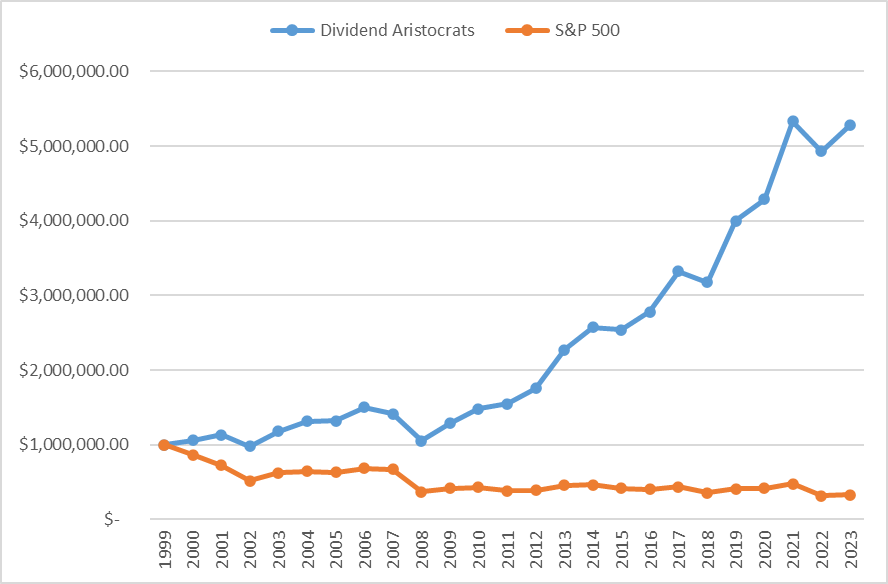

If you were unlucky enough to retire at the end of 1999 on something like S&P 500, you would not have done so well (versus Dividend Aristocrats). That’s mostly because stocks were very overvalued at the end of 1999, dividend yields on S&P 500 were very low so you were exposed to share price declines/sequence of returns risk. And worst of all, stock prices went nowhere for a decade, coupled with two gutwrenching 50%+ bear markets.

Someone who retired with $1 Million at the end of 1999 in S&P 500, using the 4% rule, would have $330,000 by the end of 2023. Someone who retired with $1 Million at the end of 1999 in Dividend Aristocrats, using the 4% rule, would have over $5.25 Million by end of 2023.

What happens if share prices decrease and or forget to increase? In the past 15 years, we’ve only seen a bull market. However during the preceding 10 or 12 years from 2000 – 2012 we saw two large 50% declines, and the share prices largely going nowhere.

Assume now that you retire at the end of the year with $2,000,000. You plan to sell $60,000 worth of stock per year, and increase that amount annually by the rate of inflation. That’s great, but by the end of the year, we are in the midst of a bear market. Share prices fall by 25%. Your $2 Million portfolio is now worth $1.5 Million. If you wanted to do a conservative withdrawal rate, you can only sell $45,000 worth of stock. But your expenses are still $60,000/year. So now you cannot retire, and have to work another year.

But somehow the next year brings a continutation of the bear market. Now your portfolio is worth $1 Million. Now your conservative 3% withdrawal would only give you $30,000. But now you actually need $61,800 per year, because of inflation.

Now you can continue waiting to retire for a few more years, until your portfolio value at a 3% withdrawal rate exceeds your expenses. The scenario is discussed is probably influenced by what I saw during the 2000 – 2012 long bear market.

If that investor had relied on a prudent diversified dividend growth portfolio for their retirement, they would have generated that $60,000 in annual dividend income in year one, then probably enjoyed some dividend growth that exceeded the 3% inflation and continued with their retirement. For as long as you have built that portfolio on a strong base, that’s well diversified, and selected good companies at attractive values to hold for the long run, the price fluctuations can be largely ignored.

These are a few thoughts I have based on my experience following investing matters for the past few years, decades etc.