I review the list of dividend increases every week, as part of my monitoring process. This exercise helps me check the pulse of dividend growth investing land. It’s a helpful exercise to check on existing holdings, and a helpful reminder to check some new companies for further research.

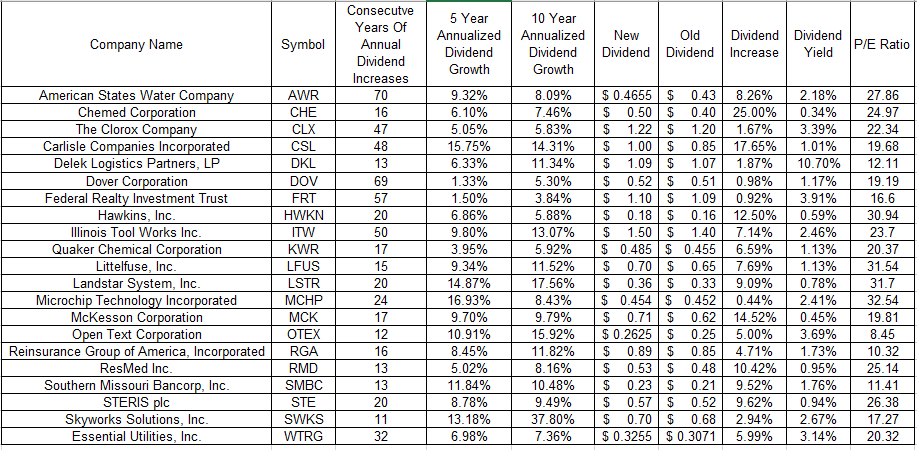

Over the past week, there were 47 companies that increased dividends in the US. Twenty-one of the companeis that increased dividends also have a ten year track record of annual dividend increases under their belt.

I have found that to be a very helpful requirement that weeds out cyclical companies.

I included the new dividend increase and calculated the rate of change relative to the last one. I also included the track record of consistent annual dividend increases.

I have also included valuation metrics such as forward P/E ratio, 5 and 10 year dividend growth rate and dividend yield.

You can view the full table below:

The companies include:

This list is not a recommendation to buy or sell stocks. It is simply a list of companies that raised dividends last week. The companies listed have managed to grow dividends for

at least ten years in a row.

The next step in the process would be to review trends in earnings per share, in order to determine if the dividend growth is on strong ground.

Rising earnings per share provide the fuel behind future dividend increases.

This should be followed by reviewing the trends in

dividend payout ratios, in order to check the health of dividend payments. A rising payout ratio over time shows that future dividend growth may be in jeopardy. There is a natural limit to dividends increasing if earnings are stagnant or if dividends grow faster than earnings.

Obtaining an understanding behind the company’s business is helpful, in order to determine how defensible the dividend will be during the next recession. Certain companies are more immune to any downside, while others follow very closely the rise and fall in the economic cycle.

Of course, valuation is important, but it is more art than science.

P/E ratios are not created equal. A stock with a P/E of 10 may turn out to be more expensive than a stock with a P/E of 30, if the latter is growing earnings and the former isn’t. Plus, the low P/E stock may be in a cyclical industry whose earnings will decline during the next recession, increasing the odds of a dividend cut. The high P/E company may be in an industry where earnings are somewhat recession resistant, which means that the likelihood of dividend cuts during the next recession is lower.

{kind=link}