Most individuals use dollar cost averaging to purchase investments. The reason behind these actions is the fact that most individuals are able to allocate funds for investing once a month or every two weeks for example, depending on the frequency with which they are able to save money. If our investor is able to save 15% of their illustrative $1000 monthly salary, which is paid every two weeks or twice/month, they would be able to allocate anywhere between $150 – $225 every month towards their retirement investments. The $225/month is derived for the situation where a person who is paid bi-weekly ends up receiving three paychecks instead of three. Either way, the typical 401 (k) investor would purchase the same funds whenever they get paid. The typical dividend investor would likely accumulate new contributions with any distributions from their portfolios, before they make their stock investments. Depending on portfolio sizes, minimum amount of purchases and amount of distributions per month, dividend investors end up purchasing different dividend stocks on a regular basis, which closely mimics the practice of dollar cost averaging.

Unfortunately, few investors have large amounts of cash simply sitting around, that they need to dollar cost average. For those lucky enough to have this happen to them, dollar cost averaging can be a tool to minimize risk of purchasing at the top. It would also help them in gaining more experience in the markets, particularly if they had none whatsoever previously. For lottery winners or those lucky individuals who happen to obtain a lump sum of cash, dollar cost averaging might be a great way to handle the bounty.

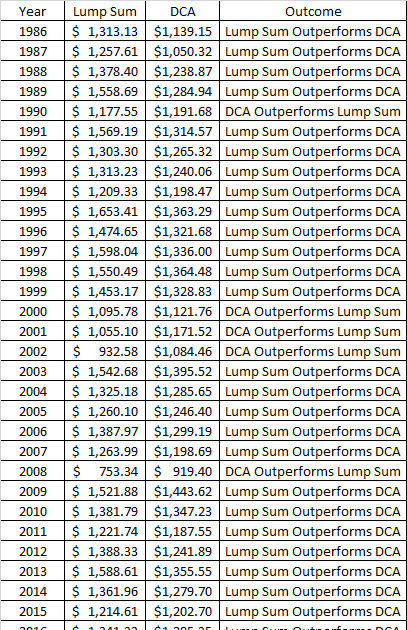

In order to test whether dollar cost averaging gives investors an advantage over lump sum investing, I obtained monthly data for the Vanguard S&P 500 mutual fund (VFINX) between 1986 and 2023. In order to calculate dollar cost averaging results for a given year, I would put $100 in investment every month beginning in the last day of the last month of the previous year, up until the last day of November for the next year. For lump-sum amounts, I would put a theoretical $1200 investment either at the closing prices for the previous year. I would then multiply the number of shares accumulated for both dollar cost averaging and lump sum investing times the ending prices by the end of the current year. Next, I would then compare which strategy delivered better results for the given year.

Overall, lump-sum investing performed better in 31 out of 38 years. Dollar cost averaging performed better in only 7 out of 38 years. Not surprisingly, these were the years when the stock market was either flat or declined. As a result, dollar cost averaging reduces investor’s risk when things were difficult, but at the expense of foregone gains when things went well. Because stocks have a historical tendency to move up over time, investors who practice dollar cost averaging might be at a disadvantage. Of course, for those who practice dollar cost averaging because they didn’t have the lump-sum in the first place, this is still the best way to accumulate a sizeable nest egg.

In this exercise we did not look at other key components of investment which deals with investment selection, analysis, valuation and purchase. We assumed that these decisions have already been made. In reality however, there could be a situation where our investor might not find any potential assets that have sufficient low valuation to merit investment in them. Most index investors or savers in a 401 (k) invest regardless of overall valuations.

Relevant Articles:

– How to accumulate your nest egg

– How to retire in 10 years with dividend stocks

– Optimal Cash Allocation for Dividend Investors

– How to Generate an 11% Yield on Cost in 6 Years

– How to be a successful dividend investor