The company earned about $11 per share in 2021 (and that is a GAAP number if you can believe it – good for them for not “adjusting” anything). So here we sit at 20x earnings, in-line with the S&P 500. So should we be bullish or bearish from here?

I think it solely comes down to whether you think the company is in a strong competitive position or not. If you believe that they have a loyal customer base and will be able to leverage the largest global streaming audience of any service, then the risk/reward looks quite attractive.

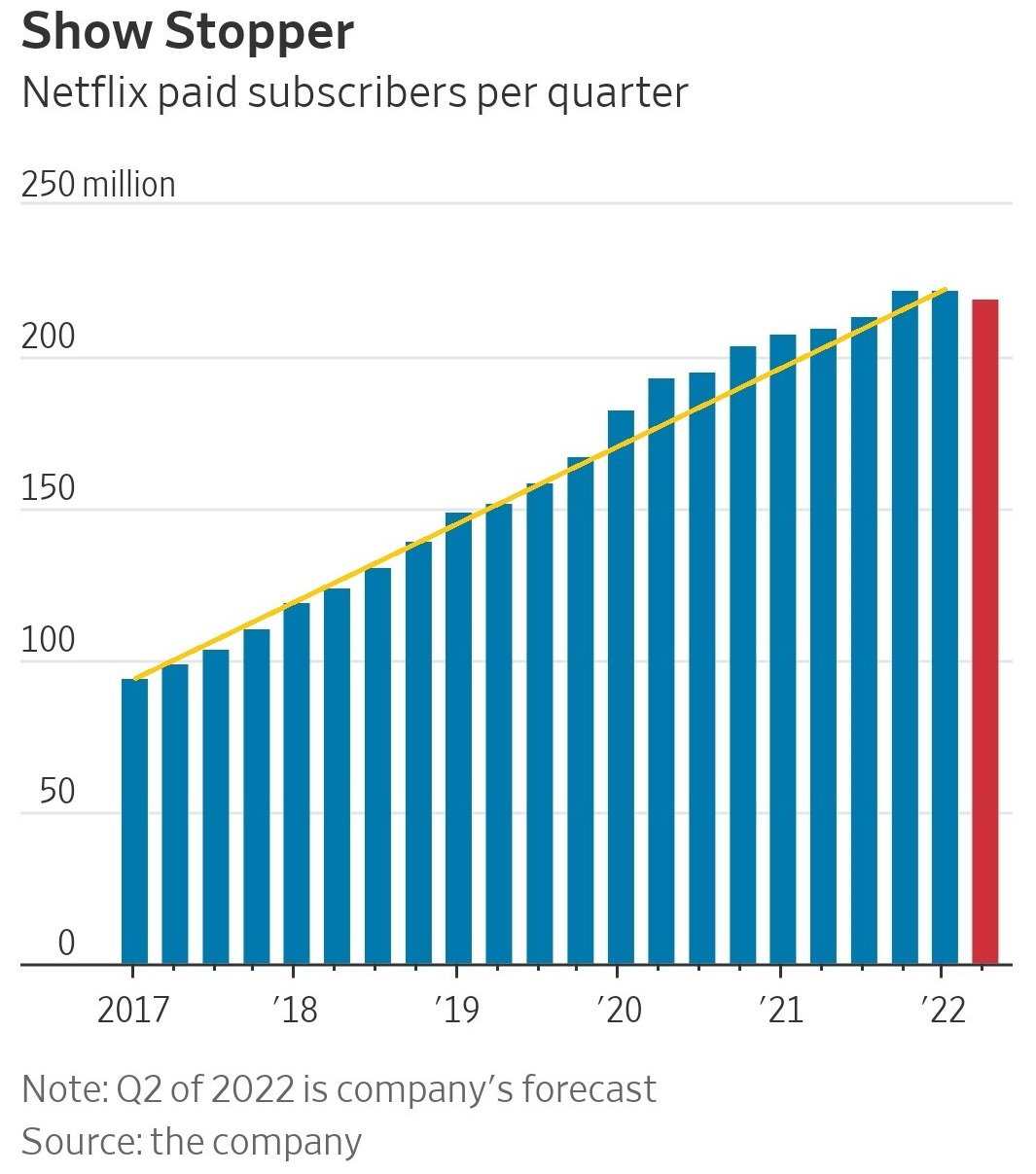

In that case, they should have pricing power into the future, be able to reasonably monetize the ~100 million households who don’t pay (they share passwords with the 220 million households who do), leverage their massive audience by introducing new offerings as time goes on, and make changes to their video service to respond to what others like Disney and HBO have done (e.g. release hit content week to week rather than all at once, add an advertising-supported tier for cost-conscious viewers and/or those who are password sharing).

My personal view is that the above factors are compelling in terms of stacking the deck in their favor now that they have reached the point where most everyone (at least in the developed markets) who wants to watch their stuff is watching.

But there is certainly a counter-argument, so let’s explore it. The bears will say that Apple, Amazon, and Disney can outspend them because they have highly-profitable business segments outside of streaming. So while Netflix was the first mover, that advantage is gone and their business has peaked. Over time, they would argue, Netflix will actually lose subscribers, rather than slowly climb towards the 300 million the bulls have always assumed was a matter of when, not if. If true, then there is no pricing power and content spend will increase more than revenue, which would be a big problem for the business, profitability, and the stock price.

Perhaps it’s too early to tell how loyal viewers are to Netflix. The success of a password-sharing monetization strategy will tell us a lot about that because if those 100 million viewers leave rather than pay a few bucks to keep watching, then Netflix probably isn’t a top tier streaming service. And if it’s not then growing earnings from the current $11 per share (and thus the stock price) will prove a difficult task.

I think they have a lot of levers to pull, but acknowledge that they need to do so thoughtfully and gently. Lastly, this is not a near-term turnaround story. Management doesn’t seem to have a full grasp on every issue they are facing coming out of the pandemic when running the business will get harder. So they will test things and evolve over time, as they have thus far. Still, at a $100 billion market cap, for the first time in a long while, the bar isn’t being set very high.

Full Disclosure: I bought some Netflix stock today at $230 per share