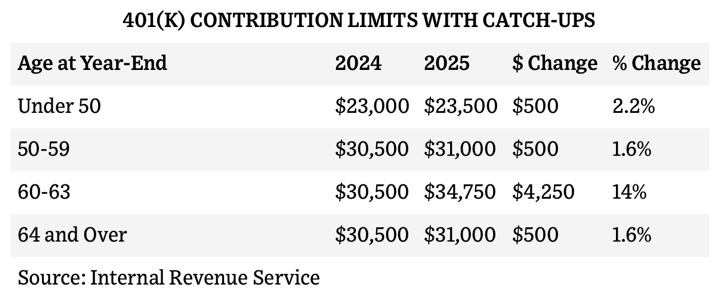

The IRS officially announced the new 401(k) contribution limits for 2025 (full news release), which also included a new “super catch-up” allowance for people who are ages 60-63 at year-end 2025. Strangely, it goes back down once you are age 64. I hadn’t heard of this before now. As usual, by “401(k)” I mean that it applies to 401(k), 403(b), governmental 457 plans, and the federal government’s Thrift Savings Plan.

The 2025 base 401(k) contribution limit is increased to $23,500, up from $23,000. This WSJ article (paywall) has a handy chart for reference.

The 2025 base IRA contribution limit remains at $7,000 (subject to income limits). Taken together, “maxing out” your IRA and 401(k) now takes more than $30,000 a year even ignoring any catch-ups. That’s a lot, but whatever you can cram in there may get roughly a 30% boost towards your final retirement balance.